A no-spend month is a short break from non-essential spending. You still pay for needs like housing, food, gas, and bills. What you pause are the extras, the impulse buys, restaurant meals, random deals, and boredom spending that add up fast. Done well, it can help you save money, spot habits you didn’t notice, and feel steadier around your finances.

This doesn’t have to be harsh or extreme. Instead, think of it as a way to press pause, make a plan, and really see where your money goes. To start your no-spend journey, focus on the first step: defining your purpose. Here’s how to do a no-spend month in a way that feels real, useful, and worth finishing.

Know Your Why

Before you set rules, think about your Why. That reason is what carries you through the hard days, not willpower alone.

Is it to build an emergency fund? Or to pay off your credit cards? Perhaps you want to save for a vacation? Or to top up your children’s educational savings?

Write your reason down. Keep it short enough to remember when temptation hits. “I want $1,000 for emergencies.” “I want to pay off my credit card.” “I want to save a start-up fund so I can start a business and eventually quit my job.”

Stick it on the fridge or someplace else where you can see it.

A no-spend challenge is challenging, that’s why it’s called a challenge. Your why has to be more powerful than your urge to spend.

Get your family on board

If you’re doing this with a partner or family, talk about the goal together. Shared goals reduce conflict later. When everyone is on the same page, the month feels less like a random restriction and more like a plan with purpose.

Make reaching your goal more fun by creating a reward. Use a sticker chart or a jar, adding a treat each day you save money. At month’s end, enjoy your collected treats.

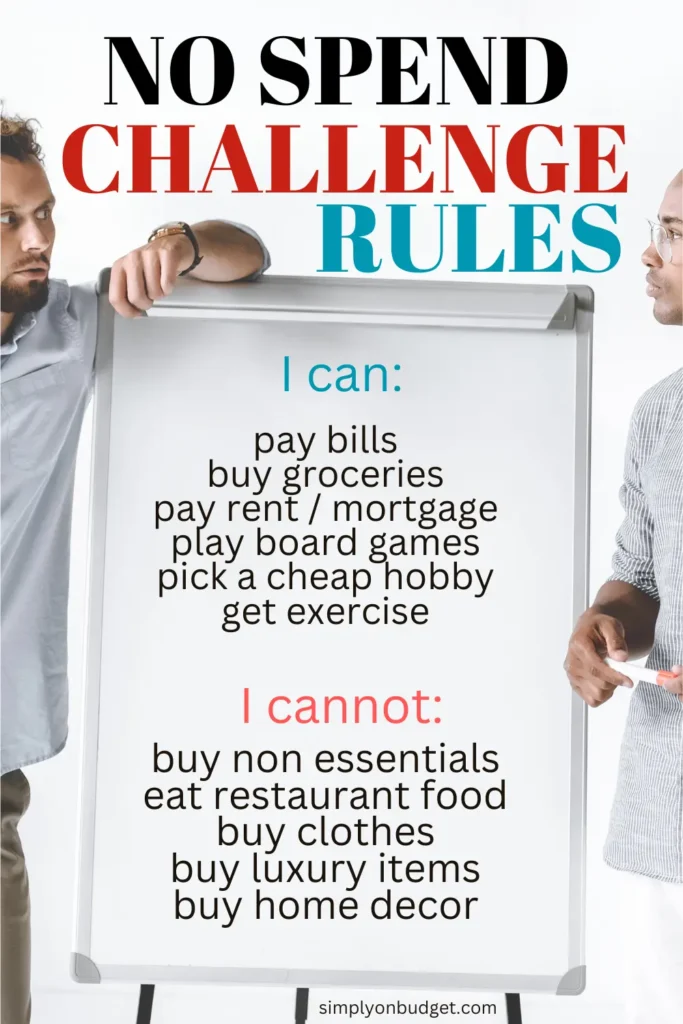

Set clear rules before your no-spend month starts

Set clear, specific rules before you begin. Deciding rules in advance prevents emotional spending during the challenge.

Pick your start and end dates. Many choose the first-to-last day of a month, but any 30-day period works. Write down your rules—memory alone is unreliable.

This quick guide helps separate the main categories:

Be very clear on what you allow yourself to spend on, and what is off-limits. Avoid the gray zones by defining them and having a plan to avoid them.

Decide what counts as essential spending

Your approved spending list should be short and boring. That’s a good sign.

Most people include housing, utilities, basic groceries, transportation, childcare, minimum debt payments, and health costs. If you use something to keep your job, care for your family, or stay safe and well, it likely belongs here.

Still, essentials are personal. A commuter may need more gas than someone who works from home. A parent may have school or child-related costs. If you manage a health condition, your list may include items another person could skip. Build your list around your real life, not someone else’s fantasy life.

Be honest about groceries—essentials don’t include treats or convenience food. Planning simple meals ahead makes the month much easier.

Check your budget planner and your calendar

Review your planned expenses for the month and plan ahead. For birthdays or events, try to make things instead of buying if possible.

Take stock of food, supplies, and subscriptions first

Start at home. Open the pantry, freezer, bathroom cabinet, and laundry shelf. Most people find more than they thought: half-used pasta boxes, canned soup, shampoo backups, stray batteries, and cleaning products hiding in plain sight. If you have children, look for board games you haven’t played in a while, craft materials waiting to be used, or other things your children would love to do that are sitting around the house because you forgot about them.

Have a meal plan and cook at home

If you don’t have a meal plan, start one now using ingredients you already have. Learn to turn leftovers into new meals.

Next, check subscriptions. Streaming services, apps, monthly boxes, premium memberships, and auto-renewals can quietly keep draining money. Pause what you don’t use. Even one or two canceled charges can make the month feel lighter. However, if you are using the subscriptions you have, definitely keep them, as they can significantly reduce your spending on activities outside the house.

Group your errands and visit as few stores as possible while shopping with a list

Always have a list made before you go shopping. Visit as few stores as possible. If it’s not on the list, don’t buy it.

Find free things to do

Having things to do takes your mind off spending. If you don’t have a hobby, pick one up.

Make a list of free or low-cost things you would like to do. Library visits, park walks, movie nights at home, game nights, free museum days, neighborhood walks, and using hobby supplies you already own all work well. Keep the list visible.

If you have children, plan even more carefully. An unplanned afternoon can turn into an expensive one. Collect your books on science experiments and crafts, and look up YouTube channels for ideas.

Clean your house and declutter

I actually find no-spend months to be the perfect time for decluttering. Deciding to reduce spending usually means going out less often, which means spending more time at home. Now that you are spending time at home, you have all the time in the world, or more precisely, an entire month, to clean your house. Go through your drawers, your children’s toys, and decide what needs to be donated, sold, or thrown away.

Make it harder to spend money

Hard days will come. Expect them. If you plan for them early, they won’t knock you over as easily.

Use tricks to stop impulse buys

Make spending a little harder. Friction helps.

Delete saved payment info from shopping sites. Unsubscribe from store emails. Unfollow accounts that constantly tempt you to buy.

Use a 7-day wait rule for anything not on your approved list.

These tricks work because they slow the gap between wanting and buying. That pause is powerful.

Handle social plans, bad days, and slip-ups with a calm mindset

You don’t need to disappear for a month. You just need to adjust the way you do things.

Invite a friend over for coffee instead of meeting at a cafe. Suggest a walk, a potluck, a free concert, or a movie night at home. Most people care more about seeing you than where you spend money.

Slip-ups may happen. One off-plan purchase doesn’t ruin the month any more than one rainy day ruins summer. Look at what triggered it. Were you tired, stressed, lonely, or caught off guard? Then adjust and keep going.

Track your wins and turn one month into lasting savings

The best part of a no-spend month isn’t only the money saved. It’s the pattern you start to see. Once those patterns are visible, you can change them.

Track both money wins and behavior wins. Maybe you skipped six takeout meals. Maybe you used food you already had. Maybe you felt less panic around money by the third week. Those changes count.

Keep a simple spending log and watch patterns show up

Use a notebook, notes app, or plain spreadsheet. Keep it simple enough that you’ll stick with it.

Write down what you spent, what you skipped, and what felt hard. You might notice that weekends trigger spending, or that stress sends you toward delivery apps. Maybe social plans are easy, but online shopping is the real problem.

Put the money saved towards your Why goals

Put the money you saved towards your goal. Otherwise, it can drift away just as easily as it came.

Don’t let the money sit in your checking account, as you’ll feel rich and want to spend it.

A no-spend month isn’t about punishment but choice. You pause, spot patterns, and decide what’s truly worth your money. Start with a clear plan and purpose. Progress isn’t about perfection—just begin.