The easiest way to start budgeting for beginners is to keep it simple: list your income, list your main bills, track basic spending, and give each dollar a job. And of course, don’t forget irregular bills and subscriptions.

This post includes a free beginners budget template. Read on to download it for free.

How to start budgeting for beginners

Think of budgeting as a mathematical equation.

Money coming in to you bank account = money going out of your bank account

Income from all sources = bills + spending + savings + investing

Budgeting is hard if you don’t know what these numbers look like. And for many of us, we just don’t bother to track how much we spend each month, or, if the income is variable, this makes budgeting much harder.

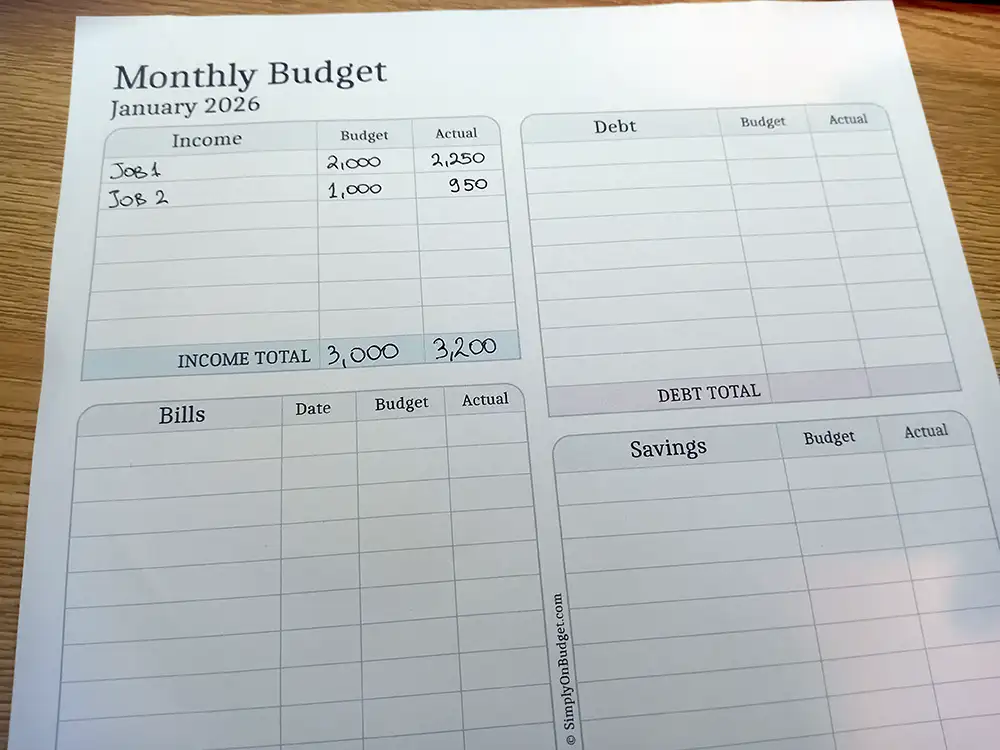

Know how much money comes in each month

Use your take-home pay, not your pre-tax salary. What lands in your bank account is the number that matters.

If your paycheck is steady, add up one month’s net income. If you’re paid twice a month, multiply one paycheck by two. If you’re paid every two weeks, use a monthly average based on recent deposits.

Irregular income needs a simpler rule. Look at the last three months, add your take-home totals, then divide by three. If your income fluctuates a lot, use the lowest recent month to keep your budget safe.

{RELATED POST: ✓How to Budget On An Irregular Income}

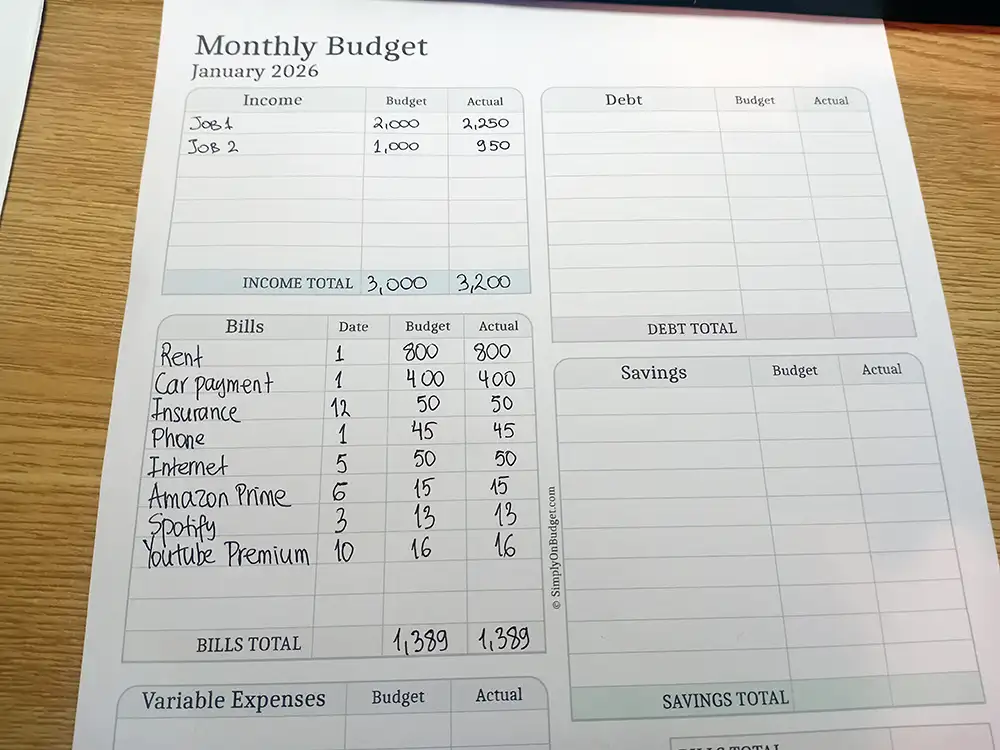

List your fixed bills before anything else

Next, write down the bills that usually stay the same and come due on a set schedule. Think rent, car payment, insurance, phone, internet, debt payments, and subscriptions you plan to keep.

These bills form the base of your budget. When you know your non-negotiables first, you lower the chance of missed payments and late fees.

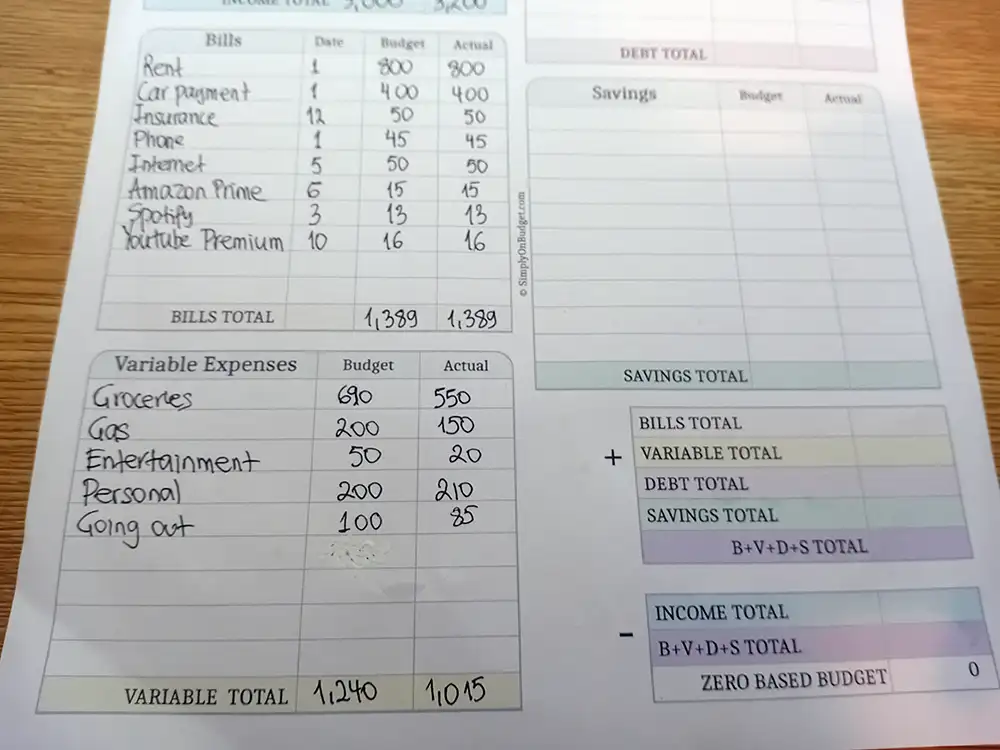

Estimate your grocery budget

This is about this as a fixed expense, even though it can vary. This is because you can’t avoid it, as you have to eat every month.

How much money do you spend on groceries each month? With the ever-increasing inflation, this number is always fluctuating. A good thing to do is to look at how much you’ve spent on groceries over the last six months, and estimate your range and average per month.

Month 1 – 550

Month 2 – 600

Month 3 – 575

Month 4 – 675

Month 5 – 600

Month 6 – 690

Your Low is: 550,

Your average is: (550+600+575+675+600+690)/6= 615

Your high is: 690.

Use simple spending buckets for everything else

After fixed bills, group the rest into a few easy buckets. Groceries, gas, eating out, fun money, and savings are enough for most beginners.

Fewer categories make budgeting easier to update. If every coffee gets its own line, you’ll quit. If food away from home goes into one bucket, you’ll keep going.

As with the grocery budget example, it’s a good idea to know your budget estimates: low, medium, and high.

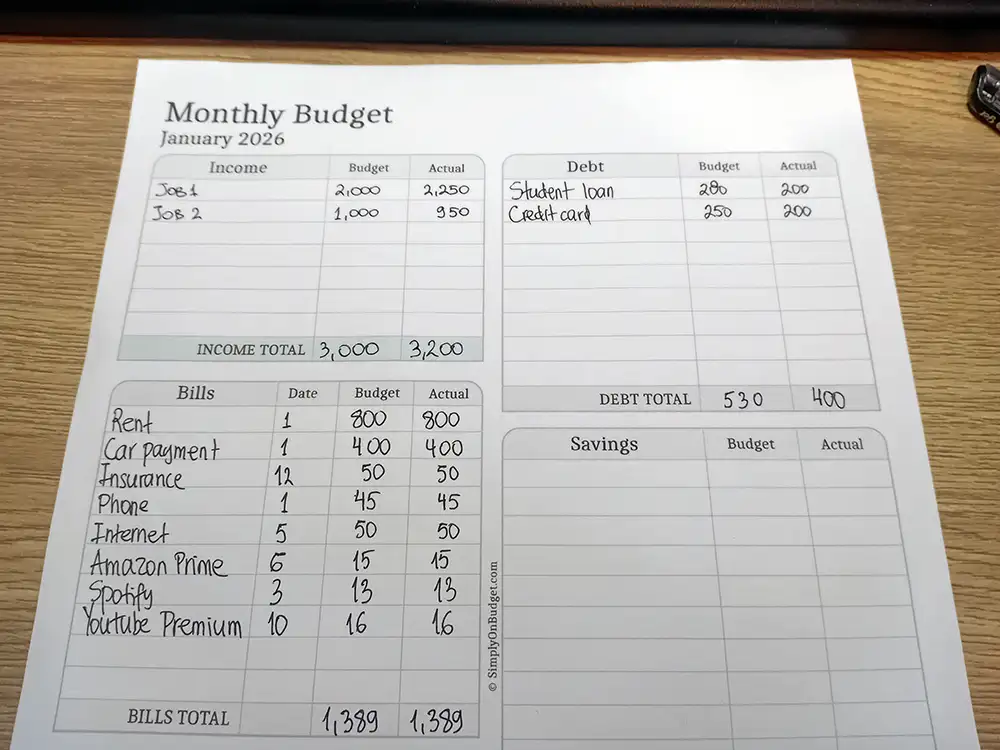

Write down your debt

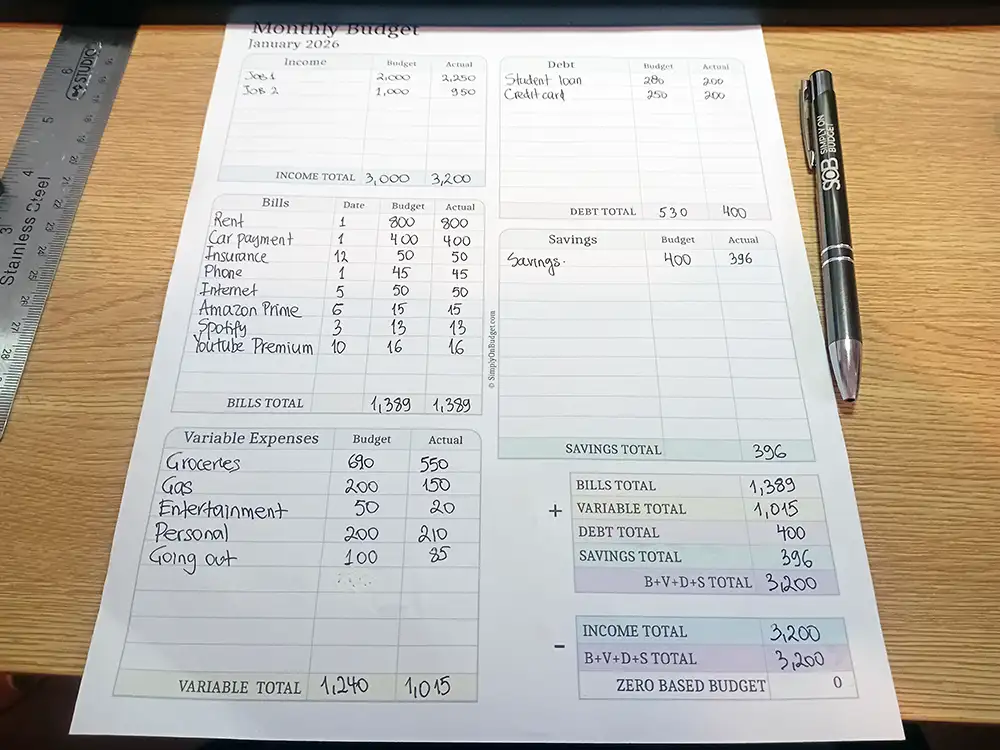

Debt is the repayment of money borrowed, and it leaves your bank account every month. Things such as student loan repayment, credit card debt. Things like ‘car payments’ are liabilities or debts to be repaid; they can also be listed under Bills because they are paid monthly. However, in a holistic financial plan, you may want to keep all liabilities under the Debt category. In this example, we wrote Car Payment under Bills because it is a fixed bill that we are repaying every month.

Write down your savings and investments

Now we are at the final section of our beginner budget. Remember, in our zero budget example, the

Income = Bills + Variable Expenses + Debt + Savings

So, in this section, our

Savings = Income – Bills – Variable Expenses – Debt

In other words, we are going to save or invest all the money left over.

So, our savings = 3,200-1,389-1,015-400 = 396

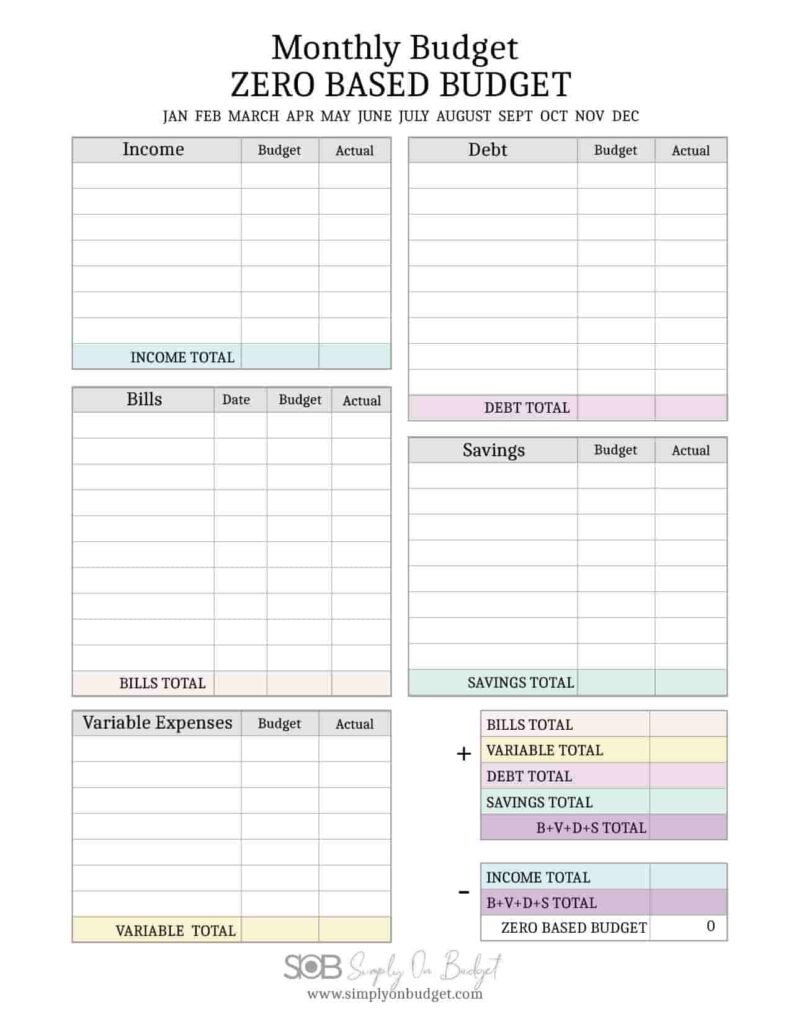

Build your first beginner budget in four easy steps

Now it’s time to make your first budget. You can do this with paper, your phone, or a basic spreadsheet.

If you like to use the template we used for our example, you can download it here. Again, this is a zero-based budget template, in which every dollar needs to be assigned a purpose.

In Summary:

Step 1: Write down income and must-pay bills

Start with the numbers that matter most. List your monthly income first, then subtract your fixed bills.

If you can, do this before the month begins. If the month has already started, do it today anyway. A late start still helps more than waiting for a perfect reset.

Step 2: Set limits for groceries, gas, and everyday spending

Look at last month’s bank activity and make rough estimates. If you spent about $400 on groceries and $120 on gas, start there.

No past records? Make your best guess. Your first budget is a draft, not a final exam. The goal is awareness, not precision.

Step 3: Include a small savings goal from the start.

Even a tiny savings line matters. Saving $10 or $25 per paycheck builds the habit early, and habits matter more than big numbers at first.

Write that savings goal under Savings – “Budget”

This money can go toward an emergency cushion, holiday spending, or car repairs. A small buffer turns money surprises into smaller problems.

Step 4: Check your budget once a week and adjust.

Budgets aren’t one-time documents. They’re living plans, and real life keeps moving.

A weekly check-in can take ten minutes. See what’s left in each category, spot problems early, and shift money if needed. That small habit keeps stress from piling up at the end of the month.

Avoid the beginner mistakes that make budgeting harder

Most people don’t quit budgeting because they’re lazy. They quit because the first plan was too strict, too detailed, or too unrealistic.

Do not make your budget too strict

If you cut every fun expense, your budget will feel like a punishment. Then one takeout meal feels like failure, and the whole plan falls apart.

Build in room for real life. A modest amount for coffee, eating out, or fun makes your budget easier to follow.

Do not forget irregular expenses

Some costs don’t show up every month, but they still count. Car repairs, birthdays, school supplies, holiday gifts, annual fees, and back-to-school shopping can wreck a tight budget.

The fix is simple. Set aside a small amount each month for these uneven costs. Then, when they arrive, they feel expected instead of painful.

Do not give up after one bad week

Overspending once doesn’t mean budgeting failed. It means your plan needs a tweak.

Reset fast. Trim another category, spend less next week, or lower a goal for this month. Progress comes from small corrections, not from being perfect.

Choose the easiest budgeting tools for your style

The best budgeting tool is the one you’ll open often. Fancy features don’t help if the system feels annoying after three days.

Paper and pen works well if you like to keep things basic

Writing things down slows you down in a good way. It helps you notice spending and stay honest with yourself.

Paper also costs almost nothing. If you want the easiest way to start budgeting today, a notebook is a good option.

A notes app or spreadsheet is great for quick updates

Digital tools make it easy to change numbers and check totals. That’s helpful when your gas bill jumps, or groceries cost more than planned.

We have a number of great budgeting spreadsheets:

Budget by Paycheck is one of my personal favorites, as it is so versatile and easy to use.

Simple 50/30/20 Budget is another great one.

A simple phone note can work well. So can a basic spreadsheet with a few lines and totals. You don’t need formulas everywhere.

Budgeting apps can help, but only if you will use them

Apps can save time by tracking spending and showing trends. Still, some beginners get lost in alerts, charts, and too many categories.

If apps feel good, use one. If they make you avoid budgeting, skip them. Simple beats fancy every time.

{RELATED POST: ✓Best Budgeting Apps for College Students}

Budgeting gets easier when you stop waiting for the perfect setup. Start with your income, cover your bills, set a few spending limits, save a little, and review once a week.

Your first budget doesn’t need to be polished. It needs to exist.

Open a notebook or your notes app today and build a basic version. A simple plan you use beats a perfect plan you never start.

{RELATED POST: ✓How to Budget On An Irregular Income}

{RELATED POST: ✓The Ultimate Beginner’s Guide to Budgeting}

{RELATED POST: ✓The Hidden Dangers of Buy Now Pay Later}