A strong credit score is a powerful asset, opening doors to better loans, housing options, and even lower insurance premiums. If your score is holding you back, don’t worry—it isn’t set in stone. With the right plan and steady effort, you can see notable improvement in as little as half a year. This guide breaks down the main drivers behind your score and offers practical, step-by-step actions to strengthen your credit profile for the long run.

{RELATED POST: ✓What’s the Easiest Way to Start Budgeting for Beginners}

Understanding Your Credit Score

It’s much easier to make progress when you understand what contributes to your score. Even though the score range for the US and Canada is not the same, and credit scores are not generally transferable between the two countries, the factors that impact your credit score and the degree to which each factor matters are very similar in both countries.

Credit Scores in the US

In the U.S., credit scores range from 300 to 850, with higher scores indicating lower risk. Generally, scores below 580 are considered Poor, scores between 580-669 are Fair, scores between 670-739 are Good, and scores between 740-799 are Very Good, and Exceptional scores fall between 800-850. The two most common Credit Score Ranges – FICO and VantageScore, help lenders assess your creditworthiness for loans and credit cards, with higher scores getting better rates.

Credit Score in Canada

In Canada, credit scores range from 300 to 900, with higher scores making you more appealing to lenders. The main credit bureaus—Equifax and TransUnion—use very similar criteria to determine your score. Generally, scores above 760 are considered excellent, 725-759 are very good, and scores below 620 are seen as subprime, impacting loan eligibility and rates.

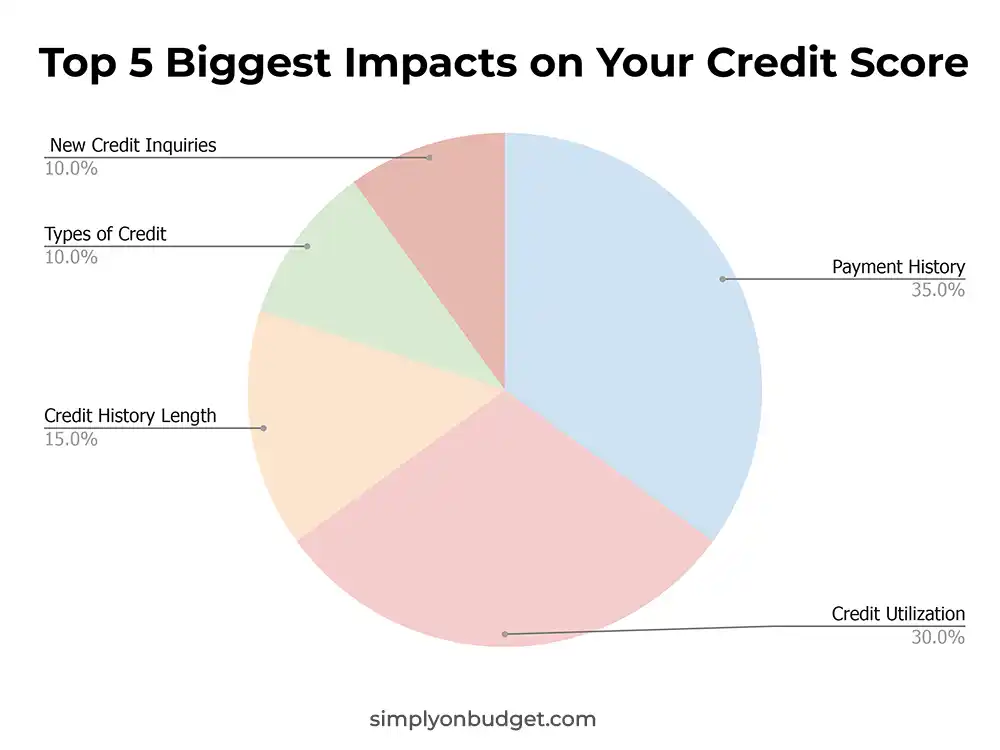

Here’s what goes into your credit score:

- Payment History (paying your bills on time) – (35%) – Have you paid your bills on time? Missed or late payments, or accounts in collections, can have a big negative effect.

- Credit Utilization (how much money you owe) – (30%) – How much of your available credit are you using? This is measured by dividing your total balances by your total credit limits. Lower is better.

- Credit History Length (how long you’ve had your credit cards) – (15%) – The longer you’ve had credit accounts open, the more data lenders have about your habits.

- Types of Credit (and other factors) – (10%) – Lenders like to see a mix of different types of credit accounts, such as credit cards (revolving), installment loans (such as car loans and mortgages).

- New Credit Inquiries (have you applied for new credit recently) – (10%) – Whenever you apply for new credit, your file gets a “hard inquiry.” Several of these in a short period can suggest risk.

Understanding these five factors provides the foundation for your six-month credit improvement journey.

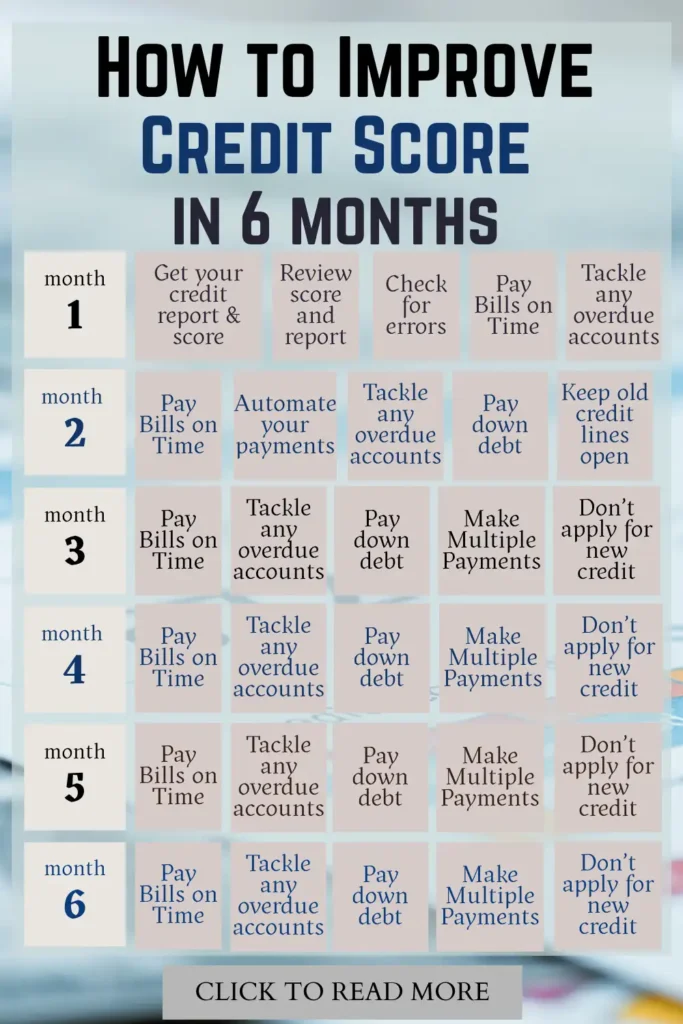

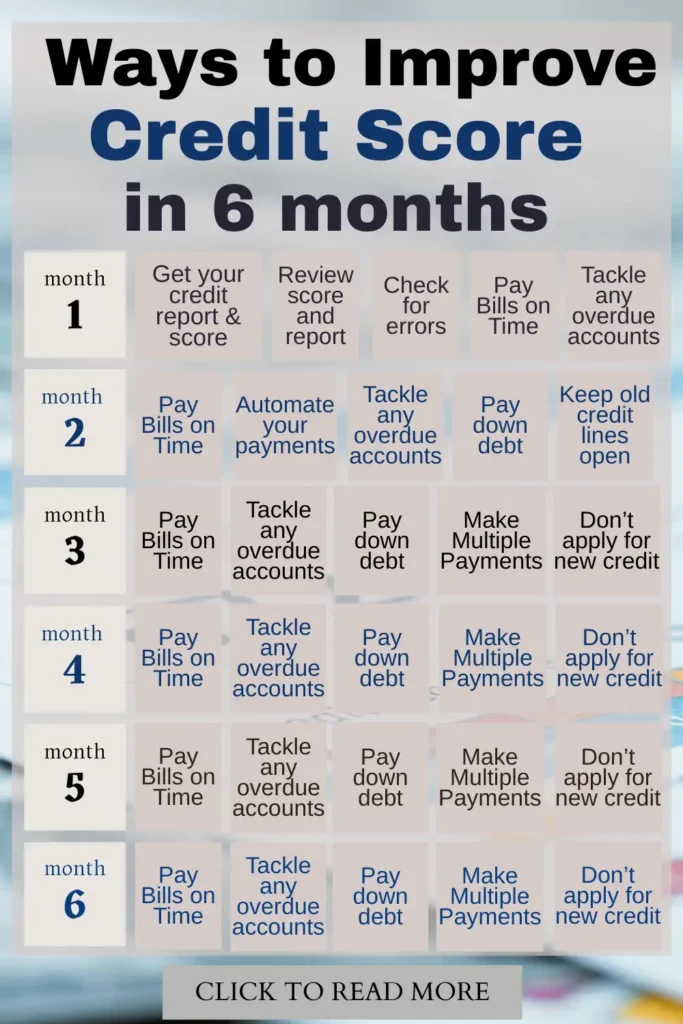

Step 1: Review Your Credit Reports and Scores (Month 1)

Start by finding out exactly where you stand. To get your free credit report in the US, go to AnnualCreditReport.com. There, you can get reports from all three bureaus (Experian, Equifax, TransUnion). You can also request free reports from both Equifax and TransUnion once per year through their websites, by mail, or over the phone. Many banks and credit card providers also offer free credit score updates in their online accounts.

As you review your report, look for:

- Your Current Standing: Take note of your score, balances, payment records, and how much credit you’re using. This is your baseline.

- Reporting Errors: Watch for incorrect account listings, payment mistakes, or personal details. Even a wrong address can signal identity errors or fraud. If you spot mistakes, dispute them with the bureau—fixing errors may quickly bump your score.

Think of this as checking your map before setting out—you need an accurate starting point to chart your progress.

Step 2: Focus on On-Time Payments (Months 1–6)

Since payment history accounts for the single largest slice of your score, it deserves top priority. A missed payment can cause lasting harm, sometimes up to seven years. In these next months, your goal is simple: pay every bill before it’s due. We have developed personal finance spreadsheets to help with debt management – try our Debt Payoff Tracker. If you are penny pinching and balancing bills by splitting them in order to juggle and pay them, try our Bills Payments tracker – it helps you do just that.

To help make that happen:

- Automate Your Payments: Use automated transfers for at least the minimum payment, or, if possible, your full statement balance.

- Set Multiple Alerts: Schedule reminders on your phone or calendar app a week and a day before each due date.

- Catch Up Quickly: If you have overdue accounts, tackle those right away. Contact creditors if you need help arranging a repayment plan, and bring the accounts up to date. Resolving these will gradually repair your history.

Building a streak of on-time payments leaves a positive mark on your record, boosting your track record with every bill.

Step 3: Lower Your Credit Utilization Ratio (Months 1–6)

Credit utilization is the share of your available credit you’re using, and lenders get nervous when it climbs above 30%. For example, with $10,000 in total available credit, try to keep balances under $3,000. Check out our post on How Not to Use Credit Cards for the most common mistakes to avoid.

To improve this:

- Pay Down Debt: Create a goal-oriented plan, such as the “avalanche” method (clear high-interest debts first) or the “snowball” method (start with the smallest balance). Pick the one that motivates you to stick with it.

- Request Higher Limits: If you’ve been making on-time payments with a card, consider requesting a limit increase. This lowers your utilization without you needing to spend less, but only if it doesn’t require a hard credit check.

- Multiple Payments: Instead of a single monthly payment, try making several smaller payments. This keeps your recorded balance lower when it’s reported to the bureaus.

These habits can help you lower your ratio and demonstrate to lenders that you manage credit responsibly.

Step 4: Keep Old Credit Lines Open (Months 1–6)

Fifteen percent of your score comes from how long you’ve had credit. Longer histories mean you’ve had more time to show responsible management. Closing an old card can hurt in two ways: it reduces the age of your accounts and your total available credit, which may spike your utilization.

Rather than closing unused cards, use each for a small recurring purchase once in a while, then pay it off. This keeps the account active and helps your score. Only close an old card if its annual fee outweighs the value it brings to your profile.

Step 5: Limit New Credit Applications (Months 4–6)

Applying for several new loans or cards in a short period means more hard inquiries, which can temporarily lower your score and flag you as a risk to lenders.

During your improvement push, try not to apply for new accounts unless absolutely necessary. If you must:

- Apply Only When Needed: Don’t take on new credit for perks or bonuses alone.

- Use Soft Checks: See if lenders offer pre-qualification tools that don’t affect your score.

- Do It All at Once: If you’re shopping for a major loan, like a car or mortgage, submit requests in a short window—credit bureaus often treat these as a single inquiry.

For the first three months, avoid applications if you can. In the final stretch, proceed only with careful planning if it helps your credit mix or lowers utilization.

Step 6: Diversify Your Credit Mix (Months 5–6)

Lenders prefer seeing a combination of credit products. If you only have credit cards, adding an installment loan (like a personal or credit-builder loan) can improve your profile’s diversity.

A credit-builder loan is designed for this purpose: you make set monthly payments, and once complete, the funds are released to you, with all payments reported to the bureaus. If taking on a new loan, make sure you can keep up with the payments without straining your budget.

Take this step later in your plan, after you’ve shown consistent on-time payments and responsible balances.

Step 7: Monitor Your Progress and Stay the Course (Months 1–6)

Improvement won’t always be instant. It may take a month or more for changes, such as paid-down balances or resolved delinquencies, to appear on your report. Use free credit monitoring apps or your bank’s credit tools to track changes over time and keep yourself motivated.

Stick with your new habits—keep making payments early, watch your balances, and avoid unnecessary inquiries. By the six-month mark, you should see your efforts reflected as a higher score and a cleaner credit report. Even more important, you’ll have built healthy routines for the years to come, putting you in control of your financial journey.

Now that you are on your way to improving your credit score, let’s examine further how to properly budget in the future to avoid falling into this pitfall again. Check out the Ultimate Beginner’s Guide to Budgeting.

{RELATED POST: ✓What’s the Easiest Way to Start Budgeting for Beginners}